Schedule Appointment »

702-660-7000

702-660-7000

There are many retirement calculators that will tell you how much you need to have in order to retire. But there are no calculators that can guarantee how much money you will need in retirement. That is because the calculators used in typical financial planning are based on some interesting assumptions. For example,

It is one thing to plan on living on 70% of your current income in retirement but quite another thing to accomplish that. Some of the reasons for that are:

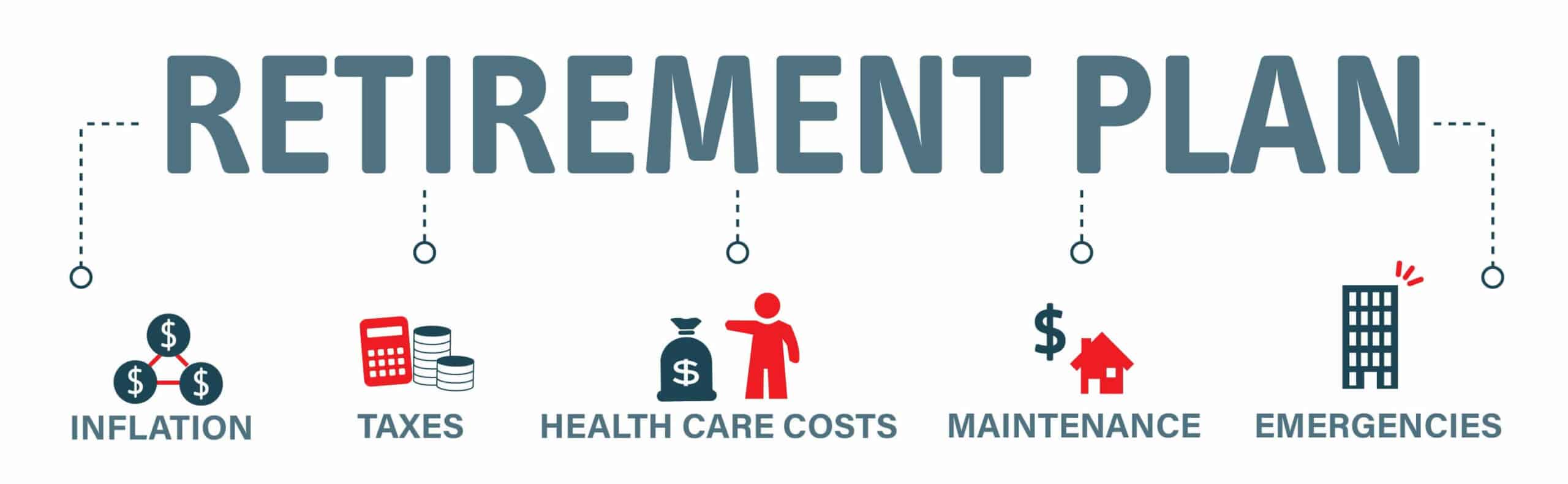

This insidious tax that everyone pays becomes more and more problematic the longer you live on a fixed income based on savings. That is because it would take $175.77 in 2020 to purchase what $100 purchased back in January of 1994. If you need $10,000 a month today to live on, but plan to live on 70% of that when you retire, then you will need $1,930,000 earning 5% annually to make it 30 years without running out of money,[i] due to inflation.

Yes, you may face taxes in retirement. The money you have kept to live on may have been tax deferred. In that case, you will pay income taxes on what you must take out of your deferred tax accounts at the time you take those distributions. If you don’t take out your required distributions from those accounts, you will forfeit 50% of what the required minimum distributions would have been to the IRS.

Earnings on investments not in qualified or tax deferred accounts will also require taxes to be paid. These may be classified as income or capital gains taxes, depending on the nature of the investment.

Of course, depending on your other sources of income, your Social Security may be taxed as well. And don’t forget state, county or local taxes that you might face in retirement, especially if you are planning on retiring to a different state than you currently live. Every state has taxes, be they sales tax, income tax, property tax, etc. Know and understand how the taxes in the state in which you plan on retiring will alter your income.

More and more Americans are needing assistance with daily living activities. Whether the cost of this needed care comes from family members or the savings of those who need the care, is a needless discussion. What is important to know is that these costs are rising. According to Genworth Financial, the average cost of assisted living for 2018 was about $48,000 a year.[ii] If you live in a northern state, you can expect to pay more and if you live in a southern state you can expect to pay less for assisted living care.

The cost of health care, for seniors, is rising. CNBC reports that from 2017 to 2026 costs are expected to rise by 5.5%,[iii] which is nearly double the cost of inflation. In 2019 a healthy male could expect to pay $135,000 over his retired lifetime on health care costs, while a female could expect to pay $150,000 over her retirement.[iv]

The big picture is, health care costs and assisted living cost are rising and will most likely continue to rise as demand rises for such services.

This is one area of living expenses that is often overlooked. Yes, the house may be paid off when you retire, but the upkeep of that property will not become any less expensive. Same with a car, or any other personal property. Everything tends to degenerate to the lowest form of order without proper maintenance. And maintenance which was easily performed by you today will most likely have to be hired done in the future.

Downsizing or budgeting for these expenditures is necessary, if you don’t want to lose money merely due to poor upkeep of assets you own.

Stuff happens in life. And the less you are able to react to circumstances the more probable it is that when stuff happens it will cost you more than when you were working and able to increase your income for emergencies or unplanned happenings.

In retirement, those little circumstances that come along could easily reduce your available resources to live on causing you to run out of money before you die. That is why participating whole life insurance is a must to have prior to going into retirement.

Participating whole life insurance is best purchased while you are young and healthy as your premiums will be lowest and remain at that low rate your entire lifetime. However, if you didn’t purchase participating whole life insurance when you were young, then the next best time to make that purchase is while you are still working.

The cash value in participating whole life insurance can be used as an emergency fund that you can depend upon without negatively affecting your income, and it could keep you from depleting your money supply and running out of money before you die.

Single premium annuities can also help assure the fact that you will have an income for the rest of your life as the insurance company issuing these contracts guarantees that you will have a specific annual, quarterly, or monthly income forever when you purchase these contracts.

Get educated about your options today, before you retire. Don’t trust the typical financial planning calculators to tell you what you need to retire. Know what expenses you will, could and might face; then plan accordingly. Many typical financial planners don’t plan for emergencies, which could leave you in your last years without any money.

Dr. Tomas P. McFie

Dr. Tomas P. McFie

Most Americans depend on Social Security for retirement income. Even when people think they’re saving money, taxes, fees, investment losses and market volatility take most of their money away. Tom McFie is the founder of McFie Insurance which helps people keep more of the money they make, so they can have financial peace of mind. His latest book, A Biblical Guide to Personal Finance, can be purchased here.

[i] https://www.nerdwallet.com/investing/retirement-calculator

[ii] https://www.seniorliving.org/assisted-living/costs/

[iii] https://www.cnbc.com/2019/04/02/health-care-costs-for-retirees-climb-to-285000.html

[iv] https://www.cnbc.com/2019/04/02/health-care-costs-for-retirees-climb-to-285000.html